The new legislative framework (which you can read more about in our briefing here) requires the development of five year carbon budgets which fix the total amount of emissions that can be emitted in the State during the five year budget period. At any one time, three sequential budgets have to be in place (although the third can be in draft form) and the three together are known as the carbon budget programme.

The Act requires that the first two carbon budgets provide for a reduction of GHGs such that annual GHG emissions at the end of 2030 are 51% less than the annual emissions at the end of 2018.

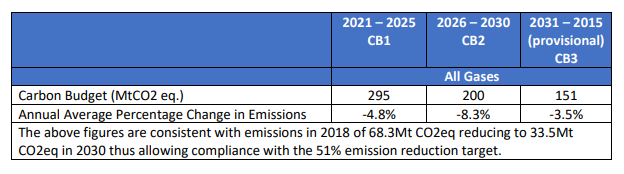

Within weeks of the new legislative framework coming into operation (on 7 September 2021), the Climate Change Advisory Council proposed carbon budgets for three successive budget periods, described by the Council as follows:

Relationship to EU Framework

Under EU law, entities (such as power plants) within sectors regulated by the EU Emissions Trading System are required to keep their emissions within EU-wide allocated caps. Allowances can be traded, with a view to ensuring that the most economically efficient abatement measures are undertaken throughout the EU, but the overall cap decreases each year.

Emission reduction targets for sectors outside the EU ETS are set at domestic level. The Effort Sharing Regulation sets reduction targets for 2021-2030 for each Member State. Under the Governance Regulation, Member States provide National Energy & Climate Plans which include information on how they will meet their Effort Sharing Regulation commitments (including strategy, objectives, policies & measures, and projected impact, including in relation to all key emitting sectors). Like all Member States, Ireland will need to revise its current NECP to reflect the more ambitious emissions reduction targets in Fit for 55, the recent EU package of legislative proposals, as well as the ambitious targets in the Programme for Government.

It will be of interest to stakeholders to understand how the EU framework is taken account of in carbon budgets and sectoral emissions ceilings in Ireland. Several features of the new framework are eye-catching.

First, it will be interesting to understand how the domestic target of reducing emissions by 51% by 2030 as against 2018 levels interacts with the European Climate Law target of reducing EU-wide emissions by at least 55% by 2030 as against 1990 levels. It had been reported that the Act targets were broadly consistent with Ireland’s NECP obligations, which suggests that the proposed carbon budgets may now not be sufficiently ambitious.

Secondly, it is not clear how targets in the Irish framework interact with the EU ETS. Individual entities who are operating in compliance with the EU ETS will be keen to understand how their existing obligations under an EU wide system are taken into account in domestic budgets or ceilings relating to them. Further clarity could help to address any potential concerns that certain sectors could be compliant with their EU obligations but nevertheless be subject to lower caps under domestic law, potentially damaging investment in Ireland without any overall benefit to EU emissions reduction.

Looking to legislative developments down the track, Fit for 55 envisages both the strengthening of the EU ETS and the combined use of emissions cap and trade with the Effort Sharing Regulation for some sectors such as fuels for road transport and buildings (described further in our briefing here). If enacted, these proposals will bring really significant change to a lot of sectors and require to be workably integrated into domestic frameworks.

Accountability for Progress

As more detail emerges, stakeholders across the economy will be keen to understand how budgets or ceilings will be enforced.

The Act obliges each Minister, in so far as practicable, to (a) perform their functions in a manner consistent with the carbon budget, and (b) in the performance of their functions comply with the sector emissions ceiling for the sector for which they have responsibility.

The Act requires relevant Ministers to attend the Oireachtas Committee on Climate Action to give an account of progress (including in relation to compliance with a sectoral emissions ceiling and any measures envisaged to address any failure to so comply). The Committee may in reply make recommendations, to which the Minister must respond. It might be speculated that it will be for the electorate to penalise poor progress, albeit hopefully without undue politicisation of the choices to be made as between individual sectors.

Next Steps

Under section 6B of the Act, the Minister within four months of receipt of the carbon budget shall cause a copy of the budget to be presented to the Oireachtas, consider the budget, amend if appropriate and finalise the budget, submit the budget to the Government for approval, and lay a copy of the budget before the Oireachtas. Not more than 30 days after a carbon budget takes effect, the Minister shall publish it. Section 6C provides for the process whereby sectoral emissions ceilings are then set.

The Government has also indicated that the Climate Action Plan 2021, another main pillar of the new climate law framework, will soon be published. These developments mark the operationalising of a domestic governance framework for climate action in Ireland that will help bring into focus the many actions needed to meet climate targets, albeit that there is still much to understand about how it interacts with EU law and policy.