WHAT is a European Long-Term Investment Fund (“ELTIF”)?

ELTIFs are specialised EU Alternative Investment Funds (“AIFs”), managed by Alternative Investment Fund Managers (“AIFMs”) authorised in line with Directive 2011/61/EU (“AIFMD”). They are intended to provide long-term finance to European infrastructure projects. Currently, an ELTIF must be an EU AIF and must be authorised by the regulator in its home jurisdiction.

When introduced in 2015, the ELTIF was a new type of regulated investment fund that invested in long-term investment opportunities and could be marketed to both professional and retail investors across the EU without being subjected to additional national requirements. The ability to market an ELTIF on a passported basis to retail investors across the EU was a significant advantage over other types of alternative investment funds, which could only be passported to market to professional investors. The ELTIF’s default closed-ended nature and long-term orientation are intended to bolster their ability to withstand market volatility, while also providing opportunities for diversification and exposure to non-traditional assets.

However, the original ELTIF legislation provided for certain protections for retail investors and the ELTIF was subject to significant limitations in terms of the types of assets that it could invest in and the diversification limits that applied. These increased compliance requirements presented significant challenges to fund promoters in terms of structuring successful ELTIF products and, as a direct result, take up of the regime was initially very low across the EU.

Following the European Commission’s public consultation on the slow uptake in ELTIFs, revisions to the ELTIF framework were proposed via Regulation 2023/606/EU (known as “ELTIF 2.0”).

ELTIF 2.0 addresses some of the major obstacles that have undermined the attractiveness of the ELTIF since it was first introduced in 2015, including significantly broadening the scope of the eligible investment universe, reducing certain investment thresholds, and removing unnecessary barriers to participation from retail investors, whilst retaining appropriate protections and diversification rules for those investing in the product. For these reasons, ELTIF 2.0 is likely to be a much more popular product than its predecessor.

WHAT is changing?

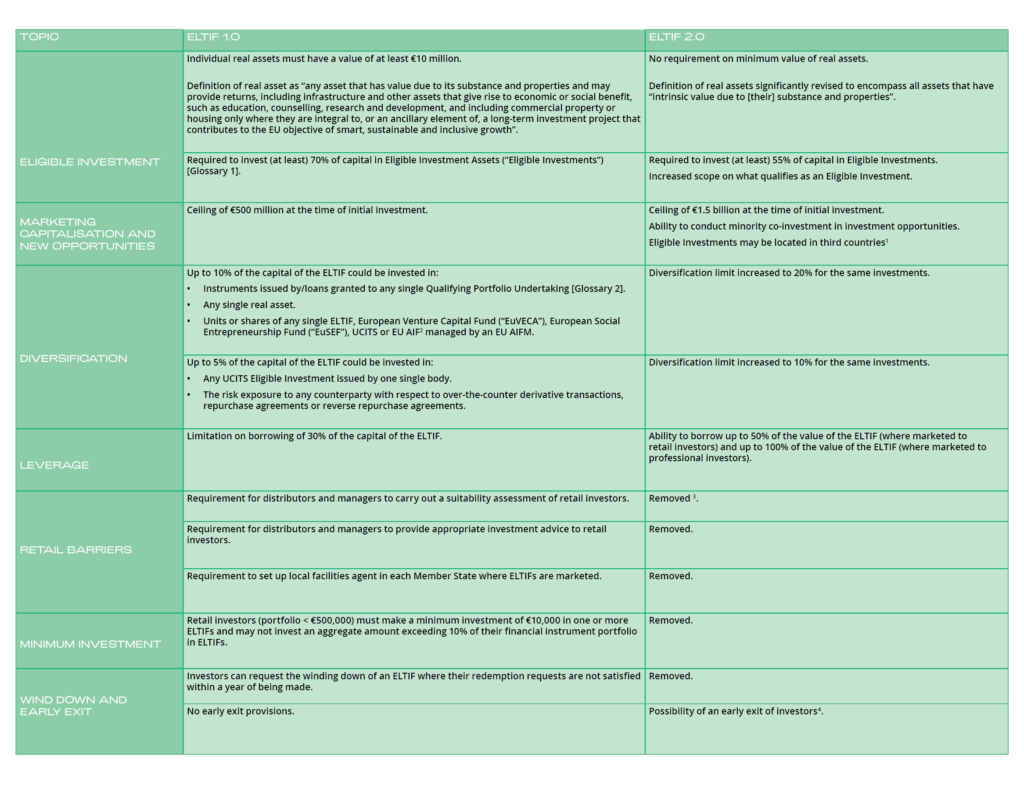

See Annex 1 for a summary of the key changes under ELTIF 2.0.

WHAT next?

ELTIF 2.0 entered into force on 9 April 2023 and will apply from 10 January 2024. In May 2023, the European Securities and Markets Authority (“ESMA”) published a consultation paper setting out proposed Level 2 regulatory technical standards (“RTS”) to supplement ELTIF 2.0. The consultation closed on 24 August 2023, and the RTS are expected to be finalised by the time the ELTIF 2.0 Regulation comes into effect on 10 January 2024.

The key to the success of this regime in Ireland will be the Central Bank of Ireland (the “Central Bank”) getting behind ELTIF 2.0 in terms of incorporating the necessary provisions in its AIF Rulebook. In this regard, industry has been engaging with the Central Bank which is in the process of developing a standalone ELTIF chapter for inclusion in the AIF Rulebook.

It is industry’s understanding that the ELTIF will be a standalone product and, therefore, it will not need to be separately authorised as a RIAIF or a QIAIF, which is very welcome. Otherwise, the authorisation process for an ELTIF is expected to broadly follow the existing authorisation processes in place for RIAIFs and QIAIFs.

Further, it is our understanding that the revised AIF Rulebook, once published by the Central Bank (which is anticipated to occur quickly and in any event prior to the end of 2023), will facilitate the authorisation of Irish ELTIFs under the ELTIF 2.0 Regulation from 10 January 2024.

If you require advice or further information on setting up an ELTIF, please contact any member of our team or your usual Arthur Cox contact.

Annex 1

Key Changes to the ELTIF Regime

1 Where those funds also invest in eligible investments and have not themselves invested more than 10% of their capital in any other collective investment undertaking.

2 Being a non-EU or non-EEA country, provided it is not identified as high-risk third country for money laundering or listed on EU list of non-cooperative jurisdictions for tax purposes.

3 Note that the suitability assessment required by MiFID II remains in force.

4 Subject to the requirement that there be a policy for matching potential investors and exit requests

Glossary

- Eligible Investment Assets (under Article 10 of ELTIF 2.0)

(a) equity or quasi-equity instruments which have been:

(i) issued by a qualifying portfolio undertaking as referred to in Article 11 and acquired by the ELTIF from that qualifying portfolio

undertaking or from a third party via the secondary market;

(ii) issued by a qualifying portfolio undertaking as referred to in Article 11 in exchange for an equity or quasi equity instrument

previously acquired by the ELTIF from that qualifying portfolio undertaking or from a third party via the secondary market;

(iii) issued by an undertaking in which a qualifying portfolio undertaking as referred to in Article 11 holds a capital participation

in exchange for an equity or quasi-equity instrument acquired by the ELTIF in accordance with point (i) or (ii) of this point (a);

(b) debt instruments issued by a qualifying portfolio undertaking as referred to in Article 11;

(c) loans granted by the ELTIF to a qualifying portfolio undertaking as referred to in Article 11 with a maturity that does not

exceed the life of the ELTIF;

(d) units or shares of one or several other ELTIFs, EuVECAs, EuSEFs, UCITS and EU AIFs managed by EU AIFMs provided that

those ELTIFs, EuVECAs, EuSEFs, UCITS and EU AIFs invest in eligible investments as referred to in Article 9(1) and (2) and have not

themselves invested more than 10 % of their assets in any other collective investment undertaking;

(e) real assets;

(f) simple, transparent and standardised securitisations where the underlying exposures correspond to one of the following

categories:

(i) assets listed in Article 1, point (a)(i), (ii) or (iv), of Commission Delegated Regulation (EU) 2019/1851;

(ii) assets listed in Article 1, point (a)(vii) or (viii), of Delegated Regulation (EU) 2019/1851, provided that the proceeds from the

securitisation bonds are used for financing or refinancing long-term investments;

(g) bonds issued, pursuant to a Regulation of the European Parliament and of the Council on European green bonds, by a

qualifying portfolio undertaking as referred to in Article 11.

- Qualifying Portfolio Undertaking (under Article 10 of ELTIF 2.0)

A qualifying portfolio undertaking shall be an undertaking that fulfils, at the time of the initial investment, the following

requirements:

(a) it is not a financial undertaking, unless:

(i) it is a financial undertaking that is not a financial holding company or a mixed-activity holding company; and

(ii) that financial undertaking has been authorised or registered more recently than 5 years before the date of the initial

investment;

(b) it is an undertaking which:

(i) is not admitted to trading on a regulated market or on a multilateral trading facility; or

(ii) is admitted to trading on a regulated market or on a multilateral trading facility and has a market capitalisation of no more

than EUR 1 500 000 000;

(c) it is established in a Member State, or in a third country provided that the third country:

(i) is not identified as high-risk third country listed in the delegated act adopted pursuant to Article 9(2) of Directive (EU)

2015/849 of the European Parliament and of the Council;

(ii) is not mentioned in Annex I to the Council conclusions on the revised EU list of non- cooperative jurisdictions for tax

purposes.