So far, so good. But what actually happens when the employer (or another party, such as its lenders) calls on a bond? What happens if the issuer of the bond – the bondsman – refuses to pay out? A recent decision of the High Court in England and Wales provides an excellent example of some of the pitfalls and how to avoid them.

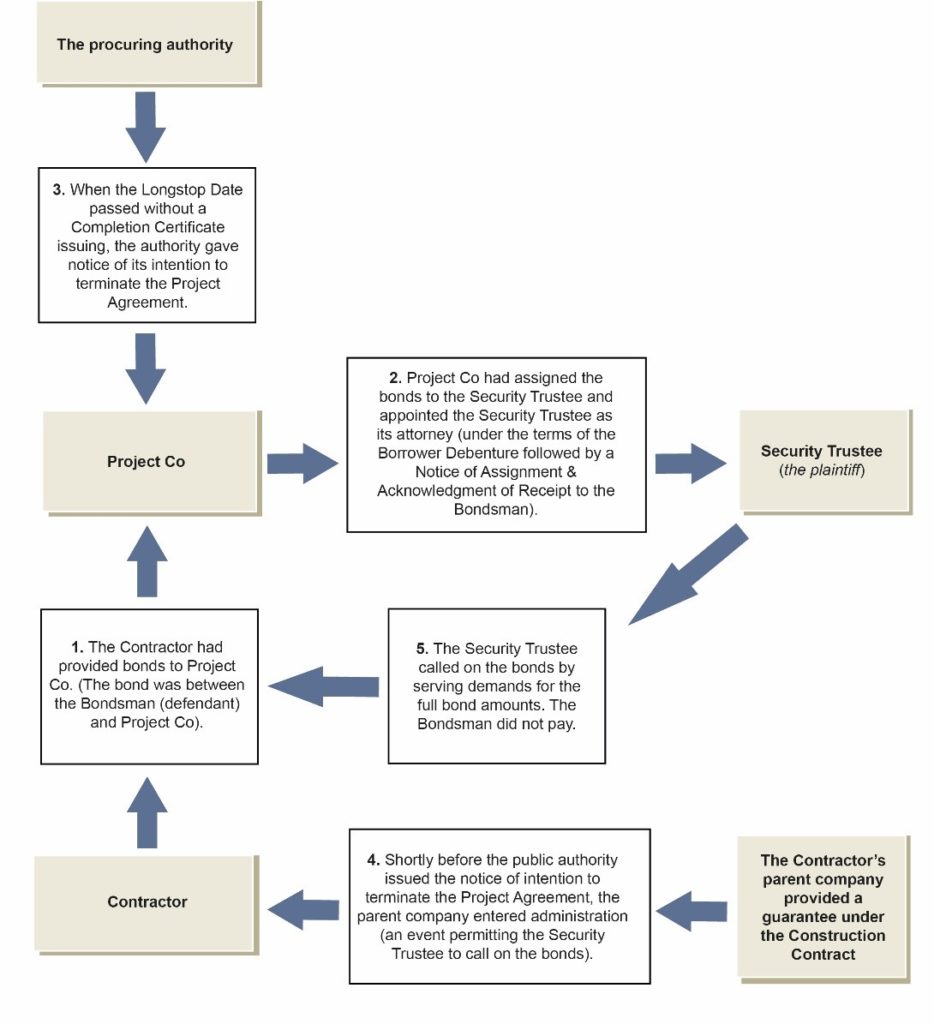

In Sumitomo Mitsui Banking Corporation Europe Limited v Euler Hermes Europe[1] a local authority was procuring waste treatment facilities through a Public Private Partnership. Project Co entered into a construction contract with the Contractor. The Contractor was required to provide a performance bond and a retention bond to Project Co. The purpose of the performance bond was to protect Project Co in the circumstances outlined in the bond (which included the insolvency of the Contractor or its parent company). The retention bond was agreed in lieu of retention monies which would otherwise have been retained by Project Co during the construction period and also gave protection in the circumstances outlined in the bond (which similarly included insolvency of the Contractor or its parent company). The Bondsman was the defendant in the litigation, Euler Hermes Europe.

In accordance with the terms of its borrower debenture, Project Co assigned the bonds to its Security Trustee (in effect its lenders) and appointed the Security Trustee as its attorney. (The Security Trustee became the plaintiff, Sumitomo Mitsui Banking Corporation Europe Ltd.) Project Co gave notice of the assignment of the bonds to the Bondsman, and the Bondsman acknowledged the notice (in respect of the performance bond, but not the retention bond).

Unfortunately, the project did not complete on time and, in early 2019, the Contractor’s parent company went into administration. The following month, the public authority gave notice of its intention to terminate its agreement with Project Co. The Security Trustee called on both bonds. The bond demands were signed twice by a director of the Security Trustee: once on behalf of the Security Trustee, and once on behalf of the Security Trustee in its capacity as attorney for Project Co. The Bondsman refused to pay and the Security Trustee sought to secure its entitlement to recover under the bonds. These facts are summarised in this diagram:

The litigation that followed is a salient reminder of the importance of paying close scrutiny to the conditions and formalities of bonds, both when agreeing them and when seeking to call on them. The main points are as follows.

- The performance bond included an obligation on Project Co at clause 8 that, if, following a court judgment, it was found that the Bondsman had paid out an amount that exceeded the Contractor’s liability, then Project Co would pay back the excess to the Bondsman. Clause 9 then said that Project Co’s assignment of the bond was subject to the assignee (who in this case was the Security Trustee) confirming to the Bondsman, in writing, its acceptance of this Project Co obligation in clause 8. The Security Trustee never did this. The Bondsman argued that, while the assignment of the bond as between Project Co and the Security Trustee was valid, there was no effective assignment vis-à-vis the Bondsman. The Security Trustee argued that the Notice of Assignment & Acknowledgment of Receipt between Project Co and the Bondsman had either been a contractual agreement that there was an effective assignment, or else a waiver of the condition in clause 9. The Court found that these arguments could not be made out to shore up the Security Trustee’s position – so the Court agreed with the Bondsman.

- What saved the day for the Security Trustee, however, was that it argued that Project Co was also entitled to call on the bond – and the Security Trustee had, as mentioned above, also signed the bond demand as attorney for Project Co. The Court accepted this.

- What is important to note is that, even though Project Co had sent the Notice of Assignment & Acknowledgment of Receipt to the Bondsman, and the Bondsman had acknowledged the assignment, the Bondsman was still able to successfully argue that the Security Trustee had not complied with its formalities – and this meant that the Security Trustee could not call on the bond in its own capacity as Security Trustee.

- The issues around the retention bond were different. There was no restriction on assignment comparable to the restriction in the performance bond and so there was no question that there had been an effective assignment. The Security Trustee could therefore call on the bond in its own right. The Court, however, went on to look at the question of whether the Security Trustee could also call on this bond as Project Co’s attorney. Unlike the performance bond, the definition of “employer” in the retention bond (who was in this case Project Co) did not extend to the employer’s “successors in title and all permitted assignees under this Bond”. Even so, the Court accepted that the Security Trustee could also call on the bond as Project Co’s attorney; on the drafting of the bond it would not make sense, when the bond contemplated that there could be assignment, for a duly authorised officer of the assignee to not also count as a duly authorised officer of Project Co. While the Security Trustee was on safer ground when it came to the retention bond, this aspect of the case provides another example of the type of scrutiny required – the impact that definitions of parties can have on capacity being the potential pitfall here.

Main Lessons

Calling on a bond is a significant event, and it is not surprising that bondsmen, notwithstanding any potential reputational impact, may take a fulsome approach to assessing whether they really need to pay out. This means that when negotiating a bond, it is vital to consider how the proposed conditions will play out when the bond is assigned or called upon. If you are assigning or calling on a bond, it is vital to pay close attention and adhere to the conditions and formalities contained in the bond. Some pointers to bear in mind are:

- Who is acting in relation to the bond and in what capacity?

- What are the formalities attaching to acting in that capacity?

- Are there deadlines by which any action has to be taken, such as giving notices? Bonds typically have an expiry date and all notices must be delivered before this date. There may also be requirements to give notice of events which may give rise to a call on the bond.

- Where must notices be served, and how? If the bondsman is located outside of Ireland, any notice formalities, such as delivery by hand, still need to be complied with.

- Are there additional requirements relating to assignment, whether express or implied, to be met?

Bonds are often similar but their provisions can vary both in terms of what damages they protect against, as well as the specific formalities for making a call. When it comes to bonds, adherence to these details is a must!

This content originally appeared in Irish Building Magazine (Issue 4 – 2019).

[1] [2019] EWHC 2250 (Comm)